Planning for the future can feel like trying to assemble a puzzle when you are missing half the pieces. For millions of American workers, homeowners, and family caregivers, two of the most critical pieces of that financial puzzle come from the exact same place: the Social Security Administration (SSA).

Yet, because both programs are run by the same agency and show up on the same statement, they are constantly confused with one another. It is common to hear people ask: “If I get hurt, should I just take early retirement?” or “Can I draw both a disability check and my regular retirement at the same time?”

To make the right choice for your family, you need a clear, plain-English roadmap. This comprehensive guide breaks down Social Security Disability Insurance vs retirement benefits, tracing exactly how they work, who qualifies for them, and how to decide which one fits your physical and financial situation. Lets deep dive into “SSDI vs. Retirement Benefits: What’s the Difference?”

READ MORE: Can Seniors on Social Security Benefits Get Free Affordable Housing?

What SSDI Is

Social Security Disability Insurance is essentially a federal safety net insurance policy that you pay into with every single paycheck via Federal Insurance Contributions Act (FICA) taxes. It is designed to replace a portion of your income if a severe medical condition prevents you from maintaining substantial employment.

The Strict SSA Definition of Disability

When looking into SSDI eligibility requirements, many people assume that “disabled” means whatever their private doctor says it means. However, the SSA operates on a very rigid, all-or-nothing standard. They do not offer partial or short-term disability benefits. To them, you are either fully disabled or you are not.

To meet the official legal definition, you must prove that:

- You cannot do the work you did before your condition began.

- The SSA decides that you cannot adjust to other types of work because of your medical issues.

- Your disability has lasted, or is expected to last, for at least one full continuous year, or is expected to result in death.

Why Your Work History and “Credits” Matter

Because SSDI is an insurance program, you must be “insured” to collect it. You earn insurance coverage by accumulating Social Security work credits when you hold a job and pay taxes.

The system relies on a calculation where you can earn up to a maximum of four credits per year. The dollar amount needed to earn a credit adjusts slightly over time based on national wage trends.

To qualify for SSDI, the general rule is that you need 40 total credits, with 20 of those credits earned in the last 10 years immediately leading up to the onset of your disability. This is often referred to as the “recent work test.”

However, the rules are more accommodating for younger individuals. If you become disabled before age 24, for example, you may qualify with as few as six credits earned in the three years prior to your condition starting.

Core SSDI Basics

- Must Have a Qualifying Disability: Your illness or injury must match an entry in the SSA’s manual of medical criteria (often called the “Blue Book”) or be equal in severity.

- Must Meet Recent Work Tests: You must have paid taxes into the system recently; you cannot sit out of the workforce for fifteen years and then suddenly claim SSDI.

- Based on Career Earnings: The actual size of your monthly check relies entirely on what you earned during your working years, not your medical bills or your current financial need.

- Not a Means-Tested Welfare Program: SSDI is entirely distinct from Supplemental Security Income (SSI). SSI is a needs-based program for people with minimal assets and income. SSDI does not care if you have savings in the bank or own a home, as long as you are not actively earning a high income from physical work.

READ MORE: How to Maximize Social Security Survivor Benefits for a Spouse

What Standard Retirement Benefits Are

Standard Social Security retirement benefits represent the classic retirement pension system that workers anticipate for decades. Unlike SSDI, which acts as emergency coverage for an unexpected life event, retirement benefits are highly predictable and structured around a sliding timeline based on your birthday.

How the Calculation Works

Your retirement benefit is calculated using your highest 35 years of indexed earnings. If you worked more than 35 years, the lower-earning years drop out of the calculation, raising your benefit. If you worked fewer than 35 years, the missing years are factored in as zeros, which can drag down your monthly average check significantly.

The Timeline Options: Early, Full, and Delayed

When it comes to the Social Security retirement age, you have choices that carry major financial weight:

- Age 62 (The Earliest Option): You can legally claim retirement benefits the moment you turn 62. However, doing so comes with a major catch. Your monthly checks will be permanently reduced by up to 30 percent compared to what you would have received if you waited a few more years.

- Full Retirement Age (The Baseline): Your full retirement age is the exact milestone where you are entitled to 100 percent of your calculated monthly benefit. Your specific full retirement age depends entirely on the year you were born. For anyone born in 1960 or later, the full retirement age is exactly 67. For those born earlier, it falls somewhere between 66 and 67.

- Age 70 (The Maximum Option): If you do not need the money immediately and choose to delay claiming your benefits past your full retirement age, the government rewards your patience. Your benefit will increase by roughly 8 percent for every single year you delay, up until you hit age 70. There is no benefit to waiting past age 70.

Crucial Reality Check: Taking your retirement benefits early at age 62 is a permanent decision. It does not automatically bump up to the full amount when you turn 67. The lower rate is locked in for the rest of your life.

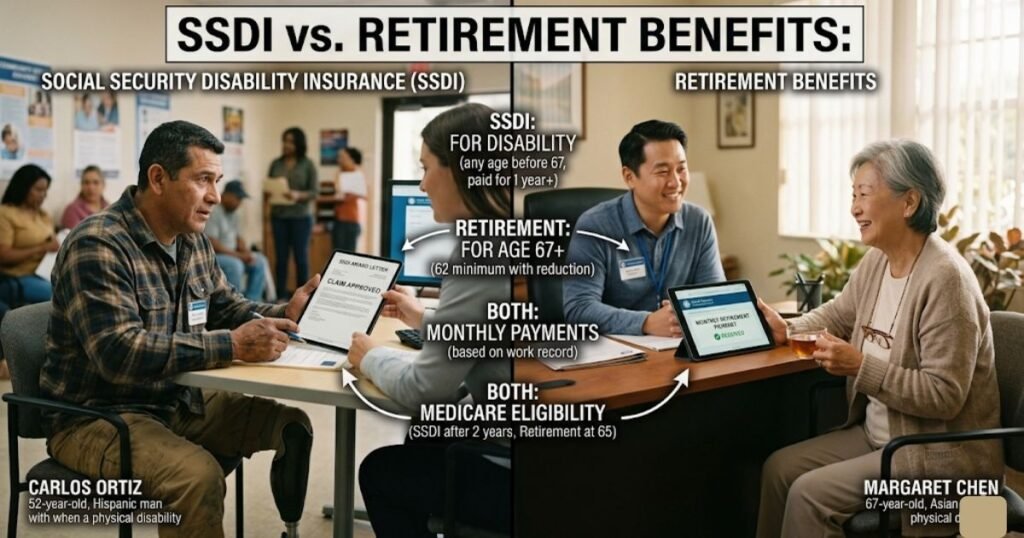

SSDI vs. Retirement Benefits

Side-by-Side Comparison at a Glance

| Feature | Social Security Disability Insurance (SSDI) | Standard Retirement Benefits |

| Primary Eligibility Basis | Severe, long-term medical disability | Attaining a specific eligible age |

| Earliest Application Age | Any age (prior to Full Retirement Age) | Age 62 |

| Work History Required | Yes (recent work plus total lifetime credits) | Yes (40 lifetime credits minimum) |

| Medical Proof Required? | Yes (extensive clinical records required) | No medical proof needed |

| Payout Amount Level | Paid at 100% of your unreduced base rate | Reduced at 62; full at Full Retirement Age |

| Impact of Early Claiming | No penalty for claiming young | Permanent monthly reduction if taken before FRA |

| Healthcare Tie-In | Qualifies you for Medicare after 24 months | Qualifies you for Medicare automatically at age 65 |

READ MORE: Difference Between Medicare and Medicaid Coverage: 2026 Guide

SSDI vs. Retirement Benefits: Which One Pays More?

If you face a health crisis near retirement age, choosing the right program significantly impacts your lifelong income. SSDI almost always pays a larger monthly check than early retirement.

Here is why: both programs start with the same baseline number your Primary Insurance Amount (PIA)—which is calculated from your lifetime earnings. However, they treat that baseline very differently if you claim before your Full Retirement Age (FRA, usually 67).

The Penalty vs. The Protection

- Early Retirement Penalty: If you claim retirement benefits at age 62, the Social Security Administration (SSA) applies a permanent reduction penalty (up to 30%) because you are drawing from the system early.

- SSDI Protection: If you qualify for disability, the SSA waives the early-claim penalty. You receive your full, unreduced baseline rate immediately, exactly as if you had successfully worked all the way to age 67.

Scenario: $2,000 Baseline Benefit at Age 62

| Pathway chosen at age 62 | Monthly Payout | The Lifelong Impact |

| Early Retirement | $1,400 | ❌ Slashed by 30% permanently for taking early distributions. |

| SSDI (Disability) | $2,000 | Receives the full, unreduced rate despite collecting early. |

READ MORE: Reverse Mortgage Line of Credit Explained: Unlock Your Home Equity

Can You Switch From SSDI to Retirement Benefits?

A common question among workers looking at their options is: “Can I get SSDI and retirement benefits at the exact same time?”

The short answer is no. You cannot “double-dip” or stack your monthly payments to get two full checks from the SSA. The system is built to provide one primary income replacement benefit at a time.

However, a smooth, automatic transition happens behind the scenes once you cross your age milestone. If you are currently receiving SSDI benefits when you reach your full retirement age, your disability benefits will automatically convert into standard retirement benefits.

What Changes During the Conversion?

- The Payment Amount: Your monthly check amount stays exactly the same. Because your SSDI was already paying you at your full, unreduced retirement rate, the transition does not cause a dip or a bump in your income.

- The Official Label: The funding pool shifts from the Social Security Disability Insurance trust fund over to the Old-Age and Survivors Insurance trust fund. To you, it simply means your benefit status changes from “disabled” to “retired.”

- The Rules Relax: Once your benefit converts to a standard retirement benefit, the strict rules regarding medical evaluations and earning limits completely disappear. The SSA will never send you for another medical review, and you can earn as much outside income as you like without worrying about losing your benefits.

READ MORE: Best Smart TV for Seniors in 2026: Easy to Use & Large Screen Picks

Common Situations Readers Face

Navigating government rules is easier when you see how they apply to real-life situations. Here are four common paths that workers and families experience.

“I am under full retirement age and became disabled”

This is the classic scenario where SSDI shines. If you are 50 years old and suffer a progressive neurological disease or a severe back injury that ends your ability to work, you should apply for SSDI right away.

Do not wait until you hit age 62 to look for options, and do not assume you have to navigate this without help. If approved, you will get your full unreduced retirement benefit amount decades early, providing vital financial stability for your household.

“I am already receiving retirement benefits and now have a disability”

If you chose to take early retirement at age 62, and then you develop a severe disabling medical condition at age 64, you can actually still apply to switch to SSDI. This is a lesser-known rule that can provide real financial relief.

If the SSA determines that your disability began after you retired but before you reached full retirement age, they can upgrade your benefit rate to the higher disability level for the remaining months until you reach age 67. This effectively erases a portion of your early retirement penalty.

“I am close to retirement age and not sure which benefit to claim”

If you are 63 or 64 and your health is failing, you might find yourself stuck in a dilemma. The SSDI application process can take many months, sometimes even years if you have to go through an appeals hearing. Early retirement, on the other hand, pays out almost immediately.

In this scenario, many people choose to apply for early retirement to get immediate income flowing into the house, while simultaneously filing an application for SSDI. If their SSDI application is eventually approved, the SSA will retroactively adjust their payments, giving them the higher, unreduced rate back to their disability onset date.

“I am helping a parent or spouse decide what to apply for”

As a caregiver, your primary job is protecting your loved one’s long-term financial health while gathering the facts. Start by checking their recent work credit history through their official online statement.

If their health issues are severe, document every doctor’s visit and treatment plan diligently. If they have the credits and meet the medical definitions, help them build a strong SSDI case rather than letting them settle for reduced early retirement checks out of sheer exhaustion.

READ MORE: Robotic Vacuum for Seniors: Best Features, Comparison, Reviews, and Buying Guide

How to Apply

Whether you are claiming early retirement or applying for SSDI, the Social Security Administration (SSA) provides three ways to file.

Application Options at a Glance

| Online Portal (Recommended) | Phone Hotline | In-Person Office |

| • Fastest method available • Save your progress as you go • Track claim status live 24/7 | • Call 1-800-772-1213 • Speak with an agent • Schedule a guided telephone filing | • Visit your local SSA branch • Best for complex document drops • Appointments highly recommended |

The Digital Route: Quick Retirement vs. Deep-Dive SSDI

Filing online via your my Social Security account is the most efficient path, but the time commitment varies wildly depending on your claim:

- Retirement Application (~15 Minutes): A straightforward, set-and-forget digital form. If you have your 40 credits and birth certificate info ready, you can submit this in one brief sitting.

- SSDI Application (Multi-Day Process): This is a rigorous medical and work-history audit. Because it requires exhaustive details on doctors, treatments, and prescriptions, the portal allows you to save your progress and return later so you can gather documents at your own pace.

Pro Tip for Offline Filing: If you prefer filing by phone or in person, call ahead to schedule an official appointment. Walking into a local field office without an appointment often results in long, exhausting wait times.

Mistakes to Avoid

- Assuming SSDI and retirement are the same thing. They are not.

- Claiming retirement too early without understanding the reduction.

- Not checking whether you have enough work credits for SSDI.

- Waiting too long to apply for SSDI if a qualifying disability is keeping you from working.

- Guessing instead of checking your situation with SSA. SSA provides online tools and application options to help you verify eligibility.

READ MORE: Best Wireless Earbuds for Senior Runners: 2026 Top Picks

Practical Tips for Readers

To put this knowledge into action, follow this simple checklist to organize your benefit strategy:

- Pull Your Official Statement Online: Head over to SSA.gov, log into your profile, and download your latest earnings statement. Verify that your yearly earnings are accurate and review your estimated benefit amounts for both disability and retirement.

- Create a Medical Documentation Log: If you plan to file for SSDI, begin gathering a comprehensive folder of your diagnoses, doctor names, clinics, hospitalizations, and prescription histories. Organization speeds up the review process.

- Run a Multi-Year Budget Projection: Compare your monthly expenses against what you would receive at age 62 (reduced retirement) versus your full unreduced disability rate. Factor in healthcare costs, especially if you need to cover insurance premiums before Medicare eligibility begins.

- Coordinate with Your Medical Professionals: Talk openly with your primary care doctors about your work limitations. Their formal clinical notes are the foundational evidence the SSA uses to evaluate your claim.

Conclusion

At the end of the day, navigating the choice between Social Security Disability Insurance and standard retirement benefits comes down to mapping your physical reality to the right legal definitions. SSDI is built to protect you when your health fails before your career naturally concludes, ensuring you receive your full unreduced baseline benefits when you need them most. Standard retirement benefits are an earned milestone based on age and a long career, offering flexibility in how and when you choose to transition out of the workforce.

Because every worker’s career path, tax history, and physical health are completely unique, never rush into a claiming decision without accurate data. Take the time to audit your earnings statement, look over your options calmly, and coordinate with the Social Security Administration to choose the path that preserves your financial peace of mind.

READ MORE: Salvation Army Free Car Program (Eligibility & How to Apply)

FAQ Section

What is the difference between SSDI and Social Security retirement benefits?

SSDI is for people who cannot work because of a qualifying disability and who have enough work credits. Social Security retirement benefits are based on age and work history, and you can usually begin them as early as 62 at a reduced rate.

Can I receive SSDI instead of retirement benefits?

Yes, if you meet SSA’s disability rules and work-credit requirements, SSDI may be the right benefit for your situation. If you are already at full retirement age, SSDI benefits generally convert to retirement benefits automatically.

Do I need to be retired to get Social Security retirement benefits?

No. SSA says you can often claim retirement benefits while still working, although your benefit may be reduced if you are under full retirement age and earn above the yearly limit.

How do I know if I qualify for SSDI?

You generally need a medical condition that keeps you from doing substantial work and is expected to last at least 12 months or result in death. You also need enough recent work credits for your age. SSA says many workers need 40 credits, with 20 earned in the last 10 years before disability begins, though younger workers may qualify with fewer.

What happens to SSDI when I reach full retirement age?

SSA says SSDI automatically converts to retirement benefits at full retirement age, and the amount stays the same. The law does not allow both benefits on the same earnings record at the same time.