Getting your financial affairs in order is one of the most reassuring gifts you can give to yourself and your family. As we get older, protecting the assets we have spent a lifetime building becomes a top priority. When exploring estate planning for seniors, you will quickly discover that standard wills often fall short of modern needs. That is where an estate planning trust comes into play.

Trusts are no longer just an exclusive luxury for the ultra-wealthy. Today, everyday retirees use a trust fund to shield their families from stress, financial leaks, and legal delays. However, one major roadblock often trips up beginners: deciding between a revocable living trust vs irrevocable trust.

This comprehensive guide will break down what you need to know in plain American English, helping you choose the path that protects your legacy and honors your family’s future. Lets deep dive into “Revocable Living Trust vs Irrevocable Trust: Complete USA Guide (2026)”

What Is a Revocable Living Trust?

A revocable trust, often referred to interchangeably as a living trust or a living trust for seniors, is a flexible legal arrangement created during your lifetime. Think of it as a magical, open box. You place your house, bank accounts, and investments inside this box, but you keep the keys.

Because you are the creator (known legally as the grantor or trustor), you retain absolute control over everything inside the box. In most cases, you also name yourself as the initial trustee, allowing you to manage the property exactly as you did before.

Key Features and Mechanics

- Total Control: You can add assets, sell property, spend cash, or remove items from the trust whenever you please.

- Complete Flexibility: You can change the terms, swap out beneficiaries, or dissolve the entire trust at any time without asking anyone for permission.

- Successor Trustee Setup: You name a trusted individual or institution to step in and manage the box if you become ill, incapacitated, or pass away.

Common Uses

Seniors primarily use a revocable living trust to simplify life for their children. It holds real estate, family heirlooms, standard taxable brokerage accounts, and cash balances to ensure they pass smoothly to the next generation.

Advantages and Limitations

The primary advantage of a revocable trust is that it morphs alongside your life. If you have another grandchild or decide to sell your home, your trust adjusts effortlessly. However, its biggest limitation is that the law views the “box” and “you” as the exact same entity. Because you maintain control, the assets are not shielded from personal lawsuits, creditors, or nursing home calculators.

READ MORE: Non Grantor Irrevocable Trust Guide: Taxes & Rules

What Is an Irrevocable Trust?

An irrevocable trust is a radically different type of legal vehicle. If a revocable trust is an open box with keys in your pocket, an irrevocable trust is a secure vault with a time-lock combination. Once you place an asset inside this vault, you walk away and hand the keys to someone else.

By definition, an irrevocable trust cannot be easily modified, amended, or canceled after it is finalized and funded. When you move your home or funds into it, you are legally giving up ownership and control for good.

Key Features and Mechanics

- Independent Management: You cannot act as the primary trustee in total control. Instead, you appoint an independent third party—like an adult child, a trusted friend, or a corporate professional to run the trust according to its written rules.

- Complete Separation: Because the assets leave your personal estate entirely, they belong to the trust itself. The trust has its own tax identification number and files separate tax returns.

- Permanent Directives: The rules you write on day one are permanent guidelines that govern how the wealth is preserved and distributed.

Common Uses

Seniors utilize irrevocable trusts for precise, high-stakes goals. The most prominent example is a Medicaid asset protection trust, designed to help seniors qualify for long-term care benefits without losing the family home. It is also utilized by high-net-worth retirees to minimize heavy tax exposure or to protect assets from high-risk legal liabilities.

READ MORE: Tax and Estate Planning Attorney Near Me

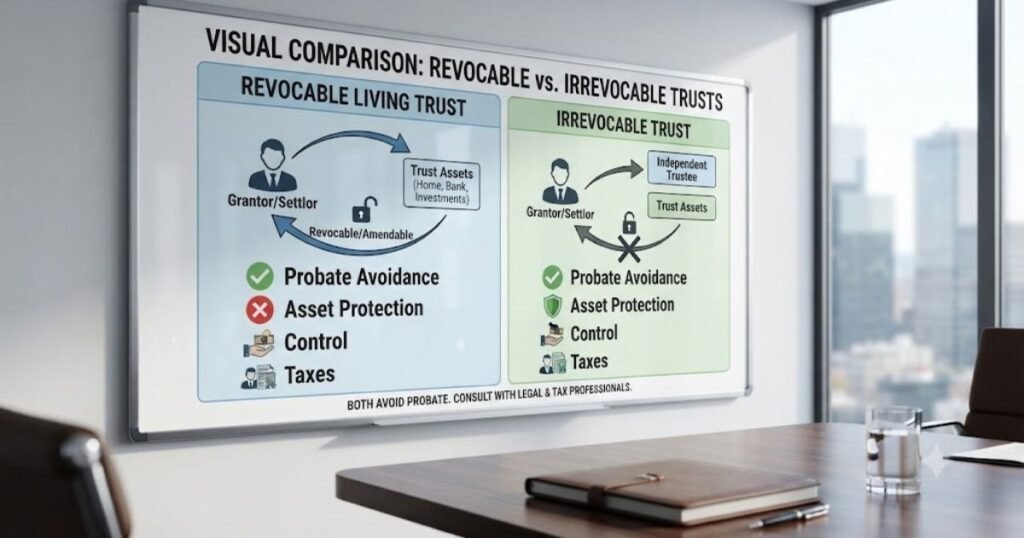

Revocable Living Trust vs Irrevocable Trust (Comparison Table)

To help visualize how these two legal tools stack up side-by-side, look at the comprehensive comparison below.

| Feature | Revocable Trust | Irrevocable Trust |

| Ownership | Kept by you (as the trustee) | Transferred entirely to the trust entity |

| Control | Full and absolute | Relinquished to an independent trustee |

| Flexibility | High; change or cancel anytime | Low; changes are rare and difficult |

| Asset Protection | None against personal creditors | Strong protection against external claims |

| Medicaid Eligibility | Counts as an available resource | Excluded from calculations (after the look-back period) |

| Estate Taxes | Included in your taxable estate | Removed from your taxable estate |

| Probate | Bypasses probate completely | Bypasses probate completely |

| Privacy | High; completely private | High; completely private |

| Cost | Moderate setup fees ($1,500 – $4,000) | Higher setup fees ($3,000 – $7,000+) |

| Complexity | Simple ongoing management | Complex administration; separate tax filings |

| Creditor Protection | No | Yes |

| Tax Treatment | Passes through to your personal 1040 | Separate tax schedules or special pass-throughs |

| Ability to Modify | Easy to amend | Requires court, beneficiary, or trust protector approval |

| Beneficiary Changes | Allowed at any time | Generally locked in, with minor exceptions |

| Best For | Probate avoidance and asset management | Long-term care planning and tax reduction |

Below is a helpful graphical summary of the foundational differences between these two common estate planning tools, highlighting their key overlapping features and distinct capabilities:

Major Advantages of a Revocable Living Trust

For the vast majority of American retirees, a revocable trust offers exactly the right mix of protection and control. Let’s look at the primary revocable trust benefits:

- Avoiding Probate: The signature advantage. When you pass away with just a will, your estate must crawl through a local court system called probate. Probate can freeze your family’s assets for six months to a year, eating up 3% to 7% of your estate’s value in administrative fees. A revocable trust bypasses this entirely, distributing your estate to loved ones almost immediately.

- Maintaining Family Privacy: A last will and testament becomes a public record once filed in probate court. Anyone can look up what you owned and who received it. A revocable living trust remains completely private; no one outside your chosen circle has a legal right to peek inside.

- Built-in Incapacity Planning: If you suffer a stroke, dementia, or a sudden medical emergency, a revocable trust shines. Your named successor trustee steps in instantly to pay your bills and manage your real estate. This completely eliminates the need for your family to fight through court for a costly, stressful guardianship or conservatorship.

- Effortless Adjustments: Life changes rapidly. A revocable trust allows you to update your plan easily if you marry, divorce, welcome new descendants, or simply change your mind about who gets what.

READ MORE: Best Estate Planning & Trust Attorneys Near Me

Major Advantages of an Irrevocable Trust

While it requires giving up control, an irrevocable arrangement unlocks powerful financial advantages that a revocable trust simply cannot touch. Consider these primary irrevocable trust benefits:

- Ironclad Asset Protection: Once property is transferred inside an asset protection trust, it is no longer legally yours. If you are sued, face a massive medical debt collection, or encounter predatory creditors, these litigants cannot seize the items inside the trust because you do not own them anymore.

- Strategic Medicaid Planning: Nursing homes and assisted living facilities are incredibly expensive. An irrevocable trust allows you to lower your countable asset total safely, letting you qualify for Medicaid long-term care support while ensuring your family home is safely preserved for your children.

- Shielding Wealth from Lawsuits: For seniors who own rental properties, ranches, or small businesses, an irrevocable setup isolates these high-liability assets from personal financial risk.

- Multigenerational Wealth Preservation: You can structure the trust so that assets stay protected from your children’s potential divorces, bankruptcies, or spendthrift habits long after you are gone.

Downsides of a Revocable Trust

No estate planning tool is perfect. To maintain maximum flexibility, a revocable trust accepts a few notable trade-offs:

- Zero Creditor Shielding: Because you can take the assets back out whenever you want, a judge can order you to do exactly that to pay off a legal judgment or debt.

- No Long-Term Care Relief: Medicaid counts everything inside a revocable trust as a personal resource. If you enter an assisted living facility, you will be forced to spend down those assets before receiving a single dime of government aid.

- No Shelter from Estate Taxes: If your estate is exceptionally large, a revocable trust does not lower your exposure to federal or state death taxes. Everything inside is valued at its full market rate upon your passing.

READ MORE: Free Wills for Seniors Near Me | Legal Help & Estate Planning

Downsides of an Irrevocable Trust

The permanence of an irrevocable agreement creates its own set of serious challenges that seniors must consider carefully:

- The Loss of True Autonomy: Once you sign over your home or money, you cannot simply change your mind, tear up the document, or pull the property back into your personal checking account.

- Reliance on a Trustee: You are completely at the mercy of the independent trustee you select. If they make poor investment choices or act uncooperatively, resolving the conflict can become an expensive administrative nightmare.

- High Setup and Maintenance Fees: These trusts require tailored drafting by a specialized trust attorney. They also demand yearly separate tax filings (IRS Form 1041), which often carry higher fiduciary tax brackets if the income is retained inside the trust.

Which Trust Protects Assets Better?

When it comes to pure defense against financial threats, the irrevocable trust wins by a landslide.

The Legal Rule of Thumb: If you have the power to change a trust, creditors have the power to crack it open. If you lack the power to change it, the law views the assets as separate property, completely out of reach from your personal problems.

Let’s look at a quick comparative breakdown:

- Lawsuits & Personal Creditors: If you are at fault in a major car accident, an aggressive attorney can pursue everything in your bank accounts and your revocable trust. An irrevocable trust, however, is a brick wall they cannot scale.

- Nursing Home Expenses: A revocable trust provides no shelter from long-term care facilities. The home inside the trust will be treated as an available asset, which may force your family to sell it to cover care bills. An properly structured irrevocable trust keeps the home safe from these facility costs.

- Bankruptcy Protection: If you fall into extreme financial distress late in life, a bankruptcy court can liquidate assets in a revocable trust to satisfy debts, while properly seasoned irrevocable assets remain shielded.

READ MORE: 8 Best Smartwatch for Hiking With GPS and Heart Rate

Revocable Trust vs Irrevocable Trust for Medicaid Planning

For many seniors, long-term care planning is the single most important factor driving their estate decisions. The central debate often centers on the revocable trust vs irrevocable trust for Medicaid calculations.

Medicaid is a joint federal and state program designed to assist with nursing home costs, but it requires applicants to have very limited assets (often less than $2,000 in countable assets for an individual).

Revocable Trust ──► Treated as personal resource ──► Must be spent down for Medicaid

Irrevocable Trust ─► Out of your name completely ──► Protected from Medicaid (if funded early)

To prevent people from simply giving away all their money the day before entering a nursing home, the government enforces a strict Medicaid look-back period. In almost every state, this look-back window is exactly five years (60 months).

If you transfer your home or retirement money into an irrevocable Medicaid asset protection trust, those assets become invisible to Medicaid only if the transfer occurred at least five years before you apply for benefits. If you enter a home four years after funding it, you will face an eligibility penalty period.

Seniors often make the mistake of waiting until a medical crisis strikes to look into this. A revocable living trust provides no help here, meaning early action with an irrevocable option is key.

Estate Tax Differences

Tax laws can feel like a moving target. In 2026, the federal estate tax landscape underwent a monumental shift due to updated legislative adjustments.

- The 2026 Federal Limit: The individual lifetime estate and gift tax exemption stands at an historic $15 million per person ($30 million for a married couple).

- Who it Affects: Because the vast majority of American families fall well under this high threshold, federal estate taxes are not a pressing concern for most.

- State-Level Reality: You must remain highly vigilant about state laws. Many states enforce their own estate or inheritance taxes with much lower triggers some starting as low as $1 million to $2 million.

A revocable living trust offers no relief from these state or federal estate taxes because the assets are still counted as part of your gross taxable estate. Conversely, an irrevocable trust removes those assets from your personal ledger. This freezes the value of the property on the day of the transfer, ensuring all future asset appreciation escapes death taxes entirely.

READ MORE: Best Smart TV for Seniors: Easy to Use & Large Screen Picks

Which Trust Avoids Probate?

Here is some excellent news: both revocable and irrevocable trusts successfully achieve probate avoidance.

When you pass away, the probate court is only concerned with assets held solely in your individual name. Because both types of trusts hold title to the assets rather than you personally, the court has no jurisdiction over them. Your successor trustee or independent trustee simply follows your written instructions to distribute the property, bypassing the public court system, saving thousands in fees, and wrapping up the administrative process in weeks rather than months.

Can You Change or Cancel the Trust?

Revocable Trust

Modifying a revocable trust is incredibly straightforward. As long as you are mentally competent, you can:

- Execute a simple amendment to alter a specific clause.

- Restate the entire trust to clean up multiple updates.

- Change your successor trustee if your original pick moves away or becomes unsuited for the job.

- Completely revoke the document if your life direction changes entirely.

Irrevocable Trust

Modifying an irrevocable trust is notoriously difficult, but it is not completely impossible in 2026. Modern estate law provides a few clever relief valves:

- Trust Decanting: Think of this like pouring old wine into a brand-new bottle. If state law allows, a trustee can pour assets from an out-of-date irrevocable trust into a newly designed one with better terms.

- Trust Protector Provisions: You can write a “Trust Protector” role into the original document. This gives an independent professional the limited power to make adjustments if tax laws shift unexpectedly.

- Judicial/Consent Modifications: If the grantor, the trustee, and every single named beneficiary sit down and agree to a change, a local court will often approve the adjustment.

Revocable & Irrevocable Trust Costs

Setting up a trust requires customized, precise legal drafting. While it costs more upfront than a basic retail store will, it saves your family immense sums down the road. Costs fluctuate dramatically based on your home state, the complexity of your finances, and your attorney’s experience.

| Service / Product Type | Average Cost: Revocable Trust | Average Cost: Irrevocable Trust |

| Attorney Setup Fees | $1,500 – $3,500 | $3,000 – $7,000+ |

| Trust Amendment | $300 – $700 | $1,000 – $2,500+ (Requires specialized consent) |

| Complete Estate Package (Includes Power of Attorney & Healthcare Directives) | $2,000 – $4,500 | $4,500 – $8,500+ |

READ MORE: Salvation Army Free Car Program (Eligibility & How to Apply)

Real-Life Examples

To see how these principles work out in the real world, let’s explore five common senior scenarios:

1. The Married Retired Couple (Bob and Linda)

- Situation: Bob and Linda own a suburban home valued at $450,000 and have $300,000 in combined retirement accounts. They want their assets to transition smoothly to their two kids without probate delays.

- Best Pick: Revocable Living Trust.

- Why: They do not have an estate tax problem, and they don’t anticipate needing immediate Medicaid assistance. They simply need control, flexibility, and a seamless transition for their children.

2. The Vulnerable Widow (Margaret)

- Situation: Margaret is 74, lives alone, and is worried about the astronomical costs of a local nursing home. She wants to ensure her beloved family home stays safe for her daughter.

- Best Pick: Irrevocable Medicaid Asset Protection Trust.

- Why: By placing her home in this trust early, she initiates the five-year look-back clock. This protects her home from being swallowed up by future medical bills, allowing her to qualify for state long-term care support down the road.

3. The Local Business Owner (Arthur)

- Situation: Arthur owns a successful regional construction supply company. He wants to slowly hand the business operations down to his son while shielding his personal savings from industry liability lawsuits.

- Best Pick: Irrevocable Trust.

- Why: Arthur needs real asset protection from business liabilities and wants to lock in a clear succession plan that isolates his personal wealth from potential company lawsuits.

4. The Family with a Disabled Child (Gary and Joan)

- Situation: Gary and Joan have an adult daughter with special needs who relies on Supplemental Security Income (SSI) and Medicaid. Leaving her money directly would accidentally disqualify her from these vital programs.

- Best Pick: Irrevocable Special Needs Trust.

- Why: This specialized version of an irrevocable trust allows them to leave funds to enhance their daughter’s quality of life without disrupting her essential government benefits.

5. The High-Net-Worth Retiree (Richard)

- Situation: Richard is a widower with an expansive portfolio of real estate and investments valued at $18 million, putting him well above individual state-level estate tax exemptions.

- Best Pick: Irrevocable Life Insurance Trust (ILIT) or Grantor Retained Annuity Trust.

- Why: Richard needs to deliberately shrink his taxable estate value to avoid leaving his children with a massive estate tax bill.

When Should Seniors Choose a Revocable Living Trust?

A revocable living trust is generally the ideal choice if you match these criteria:

- Your primary goal is ensuring your family avoids probate court.

- You want to maintain 100% control over your assets and properties.

- You expect to sell homes, move accounts, or update beneficiaries regularly.

- You want to guarantee a clear backup management plan if you fall ill.

- Your total net worth sits comfortably beneath the federal and state estate tax limits.

When Should Seniors Choose an Irrevocable Trust?

You should lean heavily toward an irrevocable structure if your situation demands these solutions:

- You are proactively planning for nursing home costs and want to qualify for Medicaid down the road.

- You work in a high-liability industry or face an elevated threat of lawsuits and debt collectors.

- Your personal estate exceeds state or federal tax thresholds, requiring you to actively shrink its size.

- You want to leave a lasting, strictly managed gift to a charitable cause or protect a special needs family member.

Common Mistakes to Avoid

Even the most well-intended estate plans can fail if you run into these classic traps:

- Failing to Fund the Trust: Creating the trust is only the first step. You must actively change the titles on your deeds, bank accounts, and investments to read in the name of the trust. A trust left empty is just an expensive stack of paper that does nothing to avoid probate.

- Choosing the Wrong Trustee: Naming your oldest child simply out of tradition can be disastrous if they are disorganized or prone to family drama. Pick a trustee based on financial responsibility, clear communication skills, and integrity.

- Ignoring Medicaid Look-Back Timelines: Waiting until you are checking into an assisted living center to build an irrevocable trust is a critical mistake. If you fail to anticipate the five-year look-back window, you may face severe eligibility penalties.

- Forgetting to Update Beneficiaries: Your trust governs what is inside it, but it doesn’t automatically override the direct beneficiary designations on your bank accounts, 401(k)s, or life insurance policies. Ensure all these individual forms match your trust’s objectives.

- Opting for Generic DIY Kits: Free online trust packages are often full of errors and fail to account for unique state-level statutes. A small mistake in drafting can easily cost your family thousands to untangle later in court.

Estate Planning Checklist for Seniors

To ensure no critical detail slips through the cracks, use this clear, practical checklist to build a robust family safety net:

- [ ] Last Will and Testament: A backup “pour-over will” to catch any loose items and sweep them cleanly into your trust at death.

- [ ] Revocable or Irrevocable Trust: Formed, signed, and fully funded with your real estate and financial accounts.

- [ ] Durable Financial Power of Attorney: Appoints a trusted person to handle your regular financial matters outside the trust.

- [ ] Advance Healthcare Directive / Living Will: Clearly details your medical care preferences and appoints a healthcare proxy.

- [ ] Beneficiary Designations: Double-check your IRAs, 401(k)s, life insurance policies, and Transfer-on-Death accounts.

- [ ] Life Insurance Review: Confirms your policies are active and align with your legacy goals.

- [ ] Digital Assets Inventory: Safely record your online login details, digital accounts, and passwords for your executor.

- [ ] Tax Planning Review: Discuss local state estate and capital gains tax brackets with a certified specialist.

- [ ] Annual Review Schedule: Set a recurring calendar reminder to review and refresh your plan after any major life event.

Frequently Asked Questions

Is a revocable living trust better than an irrevocable trust?

Neither is inherently better; they solve different problems. A revocable trust is ideal if you want absolute control over assets while avoiding probate. An irrevocable trust is best if you need to shield property from lawsuits, minimize heavy estate taxes, or protect your home from nursing home costs.

What are the disadvantages of an irrevocable trust?

The primary disadvantage is a total lack of flexibility. Once assets transfer, you surrender personal control and cannot easily alter beneficiaries or dissolve the trust. Additionally, they are expensive to establish, require an independent trustee, and must file their own annual IRS tax returns.

Does a revocable trust protect assets from nursing home costs?

No, it offers absolutely no protection against long-term care costs. Because you retain the power to alter or cancel the trust at any time, government agencies like Medicaid count these assets as personal resources. You must spend them down completely before qualifying for state nursing home assistance.

Can a revocable trust become irrevocable?

Yes, a revocable trust automatically becomes irrevocable when you pass away. Because you are no longer alive to alter or revoke the document, the terms become permanently locked. Your appointed successor trustee then takes over to manage and distribute the assets exactly as you originally directed.

Which trust is best for avoiding probate?

Both revocable and irrevocable trusts are equally excellent at avoiding probate. Because both types hold legal title to your assets, the property does not form part of your individual estate upon death. Your designated trustee can transfer everything to loved ones quickly and privately, completely bypassing court.

Conclusion

When organizing your estate, there is no single right answer. The ideal choice depends on your personal net worth, your immediate health trajectory, and your family goals.

For many seniors, a revocable living trust delivers the perfect balance of probate avoidance and lifelong financial control. But if your priorities focus on long-term nursing care protection or minimizing tax exposure, stepping up to an irrevocable trust can secure your legacy.

Because trust laws vary significantly by state and individual financial situations, you should never attempt a DIY approach. Reach out to a qualified trust attorney or estate planning specialist in your local area to design a personalized plan that keeps your wealth secure and your family protected.