If you are a senior living in America today, you know that your dollar doesn’t stretch quite as far as it used to. Whether it’s the rising cost of healthcare or the price of groceries, managing a fixed income requires careful planning. Fortunately, recent changes to the U.S. tax code have introduced a significant new benefit designed specifically to keep more money in your pocket.

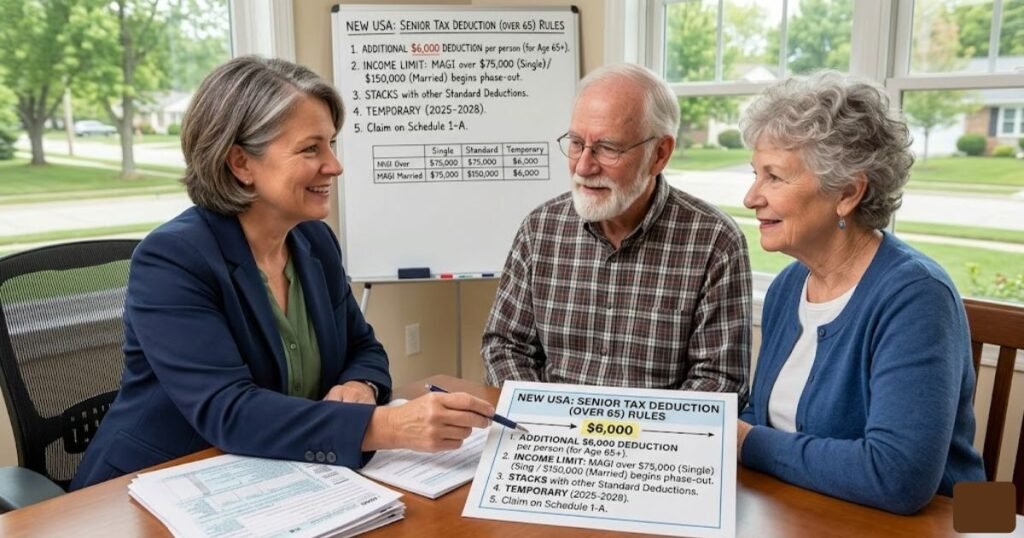

The $6,000 senior tax deduction often called the “Enhanced Senior Deduction” is one of the most substantial tax breaks for retirees in decades. Established under the “One, Big, Beautiful Bill” (OBBB) passed in 2025, this provision is now in full swing for the 2026 tax year.

If you are 65 or older, understanding the 6000 Dollar Senior Tax Deduction for Over 65 Rules is essential. This guide will walk you through everything you need to know, from eligibility requirements to how this deduction “stacks” with your existing benefits.

READ MORE: Robotic Vacuum for Seniors: Best Features, Comparison, Reviews, and Buying Guide

What Is the $6,000 Senior Tax Deduction?

At its core, the $6,000 senior tax deduction is a federal provision that allows eligible taxpayers age 65 and older to reduce their taxable income by a flat amount of $6,000 per person.

It’s a Deduction, Not a Credit

It is important to understand the difference between a tax deduction and a tax credit.

- A Tax Deduction reduces the amount of your income that is subject to tax. If you are in the 12% tax bracket, a $6,000 deduction “saves” you roughly $720 in actual taxes owed ($6,000 x 0.12).

- A Tax Credit would reduce your tax bill dollar-for-dollar.

While a credit might sound better, a $6,000 deduction is still a massive win because it lowers your Adjusted Gross Income (AGI), which can help you qualify for other benefits and lower the portion of your Social Security that is taxed.

A New Layer of Savings

The most important thing to know is that this is not the same as the “extra” standard deduction you might already be familiar with. For years, seniors have received a slightly higher standard deduction than younger taxpayers. This new $6,000 benefit is in addition to that.

For the tax years 2025 through 2028, the maximum amount is:

- $6,000 for a single eligible person.

- $12,000 for a married couple if both spouses are 65 or older.

READ MORE: Home Equity Line of Credit vs Reverse Mortgage: A Guide for U.S. Senior Homeowners

Who Qualifies $6,000 Senior Tax Deduction? (Eligibility Rules)

The IRS has kept the eligibility rules for the senior tax deduction over 65 relatively straightforward to ensure that as many retirees as possible can benefit. However, there are three primary “hoops” you must jump through.

1. The Age Rule

To claim the deduction, you must be 65 or older by the last day of the tax year. For the 2026 tax year, this means you must have celebrated your 65th birthday on or before December 31, 2026.

Pro Tip: The IRS considers you to be 65 on the day before your 65th birthday. If your 65th birthday falls on January 1, 2027, the IRS considers you 65 as of December 31, 2026, meaning you still qualify for the 2026 tax year!

2. Filing Status

The deduction is available to:

- Single filers

- Head of Household filers

- Married Filing Jointly

- Qualifying Surviving Spouses

Note: Currently, the deduction is generally not available for those using the Married Filing Separately status. If you and your spouse file separately, you should consult a tax professional to see if the benefits of filing jointly (to claim the $12,000 total) outweigh your current strategy.

3. Income Limits (The Phaseout)

The IRS senior deduction rules include an income cap. The deduction is designed to help low-to-middle-income seniors. As your income rises, the deduction begins to “phase out” (gradually disappear).

The phaseout begins when your Modified Adjusted Gross Income (MAGI) exceeds:

- $75,000 for single filers.

- $150,000 for married couples filing jointly.

If your income is below these amounts, you get the full $6,000 (or $12,000). If it is above, the deduction is reduced by 6 cents for every dollar you earn over the limit until it reaches zero.

READ MORE: Best Wireless Earbuds for Senior Runners: 2026 Top Picks

How the Deduction Works With the Standard Deduction

One of the biggest points of confusion for seniors is whether they have to choose between this new $6,000 amount and the “Standard Deduction.”

The answer is: You get both.

In the past, tax breaks for seniors were often tied specifically to the Standard Deduction. If you itemized your deductions (for things like high medical bills or mortgage interest), you lost the senior “bonus.”

The $6,000 senior tax deduction is different. It is a “below-the-line” deduction available to everyone who qualifies, regardless of whether you:

- Take the Standard Deduction.

- Itemize your deductions on Schedule A.

The “Stacking” Concept

Think of your tax breaks like a layer cake.

- Layer 1: The Base Standard Deduction (available to all taxpayers).

- Layer 2: The Additional Standard Deduction for Age 65+ (the “old” senior bonus).

- Layer 3: The New $6,000 Senior Tax Deduction.

When you stack these together, a single senior in 2026 can shield nearly $25,000 of income from federal taxes before they owe a single penny.

READ MORE: How to Switch From Medicare Advantage to Medigap

Comparison Table: Senior Tax Benefits 2026

To help you visualize how these different benefits interact, here is a breakdown of the primary senior tax benefits available in 2026.

| Tax Benefit | Who Can Claim It | Maximum Amount (Approx) | Income Limits | Purpose |

| Standard Deduction | Most taxpayers | ~$16,000 (Single) / ~$32,000 (Joint) | None for most | Reduces overall taxable income. |

| Addtl. Standard Deduction (65+) | Seniors age 65+ | ~$2,000 (Single) / ~$3,200 (Joint) | None | Extra benefit for being 65+. |

| New $6,000 Senior Deduction | Seniors age 65+ | $6,000 per person | Starts phaseout at $75k/$150k | New 2025-2028 added relief. |

| Itemized Deductions | Those with high expenses | Varies by expenses | Depends on expense type | Use if higher than standard deduction. |

| Credit for Elderly/Disabled | Low-income seniors | Up to $7,500 | Very low income limits | Direct reduction of tax bill. |

Married Filing Jointly: How Couples Qualify

If you are married and both you and your spouse are over 65, the news is even better. The $6,000 senior tax deduction applies to each person.

If Both Spouses Are 65+

A married couple filing jointly can claim a combined deduction of $12,000. When you combine this with the 2026 standard deduction (estimated at over $33,000 for a senior couple), your household could potentially have over $45,000 in tax-free income.

If Only One Spouse Is 65+

What if you are 67 but your spouse is 62?

In this case, you can still claim the deduction, but only for the eligible person. Your household would receive a $6,000 deduction. Your spouse will become eligible for their own $6,000 deduction once they reach age 65, provided the law is still in effect (it is currently set to run through the 2028 tax year).

READ MORE: Best Smart TV for Seniors in 2026: Easy to Use & Large Screen Picks

Income Phaseout Explained Simply

The “Phaseout” is a term the IRS uses to describe a benefit that slowly shrinks as you make more money. It’s not a “cliff” where you lose everything the moment you make $1 over the limit. Instead, it’s a gradual reduction.

An Easy Example

Let’s say you are a single filer named Robert.

- Robert’s Age: 70

- Robert’s MAGI: $85,000

- The Threshold: $75,000

Robert is $10,000 over the limit ($85,000 – $75,000 = $10,000).

The IRS rule states the deduction is reduced by 6% (or 6 cents) for every dollar over the limit.

- $10,000 x 0.06 = $600 reduction.

- Full Deduction ($6,000) – Reduction ($600) = $5,400.

Even though Robert earns more than the $75,000 limit, he still gets to keep $5,400 of his deduction. The deduction doesn’t disappear entirely until a single filer’s income reaches $175,000 (or $250,000 for a married couple).

Step-by-Step: How to Check If You Qualify

Ready to see if you can claim the $6,000? Use this simple checklist:

- Verify Your Age: Were you 65 or older on Dec 31, 2026? (If yes, move to step 2).

- Confirm Filing Status: Are you filing as Single, Head of Household, or Married Filing Jointly? (Avoid Married Filing Separately).

- Calculate Your MAGI: Look at your total income (Social Security, pensions, 401k withdrawals). For most seniors, your MAGI is very close to your Adjusted Gross Income (AGI).

- Compare to Limits:

- Single: Is your MAGI under $75,000?

- Married: Is your MAGI under $150,000?

- Check Your SSN: Ensure you have a valid Social Security number for work, which is a requirement for this specific deduction.

- Decide on Itemizing: Calculate if your itemized deductions (medical, etc.) are higher than the standard deduction. Remember, you get the $6,000 regardless!

READ MORE: Best Wireless TV Headphones for Seniors (2026) – Clear Sound & Easy Setup

Common Mistakes Seniors Should Avoid

When a new tax rule like the age 65 tax deduction is introduced, it’s easy to get confused. Here are the most common pitfalls to watch out for:

- Assuming it’s a Refund: A $6,000 deduction is not a $6,000 check in the mail. It reduces your taxable income, which in turn reduces the tax you owe.

- Forgetting the Income Limit: If you have a high income (e.g., you are still working a high-paying job or took a large RMD from an IRA), your deduction might be smaller than $6,000.

- The “Married Filing Separately” Trap: Many couples file separately for various reasons, but doing so will likely disqualify you from this specific $6,000 benefit.

- Confusing the Two Senior Deductions: Don’t forget to claim the other additional standard deduction for being 65+. Some seniors think they have to choose one or the other, but they are separate benefits.

- Missing the Deadline: This deduction is temporary! It applies for tax years 2025, 2026, 2027, and 2028. If you don’t claim it now, you might miss out before the law expires.

Other Senior Tax Benefits to Know

While the $6,000 deduction is the “star of the show” in 2026, don’t overlook these other ways to save:

1. Medical Expense Deductions

If you itemize, you can deduct medical expenses that exceed 7.5% of your AGI. For many seniors, this includes long-term care insurance premiums, hearing aids, and even home modifications for accessibility.

2. Qualified Charitable Distributions (QCDs)

If you are 70½ or older, you can donate up to $100,000 (indexed for inflation) directly from your IRA to a charity. This counts toward your Required Minimum Distribution (RMD) but isn’t counted as taxable income. This is a great way to keep your MAGI low so you can qualify for the full $6,000 senior deduction!

3. Credit for the Elderly or the Disabled

This is a tax credit for those with very low incomes. If your income is low enough, this credit can wipe out your tax bill entirely.

4. Property Tax Relief

Many states offer “Senior Freeze” programs or homestead exemptions that lower your local property taxes once you turn 65. While this isn’t a federal IRS rule, it’s a vital part of a senior’s financial plan.

READ MORE: Best OTC Hearing Aids for Tinnitus (2026) | Affordable & Effective Picks

Conclusion:

The 6000 Dollar Senior Tax Deduction for Over 65 Rules represents a significant effort by the government to provide relief to retirees. By allowing you to shield an extra $6,000 (or $12,000 for couples) from taxes, the IRS is making it easier for seniors to manage their cost of living in 2026.

The best part of this deduction is its flexibility—it doesn’t matter if you take the standard deduction or itemize your medical bills, the $6,000 is there for you as long as you meet the age and income requirements.

As always, tax laws can be complex and are subject to change. While this guide provides a clear overview for 2026, it is always a smart move to consult with a certified tax professional or use reputable tax software to ensure you are maximizing every dollar you’re entitled to.

Frequently Asked Questions (FAQ)

What is the $6,000 senior tax deduction for people over 65?

It is a federal tax deduction enacted in 2025 that allows taxpayers age 65 and older to reduce their taxable income by up to $6,000 per person. It is available for the tax years 2025 through 2028.

Who qualifies for the new senior tax deduction?

To qualify, you must be 65 or older by the end of the tax year and meet certain income requirements. The full deduction is available to single filers with a MAGI under $75,000 and married couples under $150,000.

Is the $6,000 senior deduction separate from the standard deduction?

Yes. This is a “below-the-line” deduction that stacks on top of the standard deduction. You can claim it whether you take the standard deduction or choose to itemize your deductions.

Does the senior deduction phase out at higher income levels?

Yes. The deduction begins to decrease once your income passes $75,000 (Single) or $150,000 (Married Filing Jointly). It is reduced by 6 cents for every dollar over those limits.

Can married couples claim $12,000 if both spouses are over 65?

Absolutely. If both spouses meet the age requirement and the couple files a joint return, they are eligible for a combined deduction of $12,000, provided they fall within the income limits.

READ MORE: Salvation Army Free Car Program (Eligibility & How to Apply)